Dec 12

preview

Toggle AI is now Reflexivity! Click here to go to our new website

TLDR: In the latest chapter of the U.S. monetary saga, the Fed kept interest rates unchanged, resisting the temptation to alter its course despite ongoing inflation worries.

Holding the federal funds rate at 5.25% to 5.5%, the decision mirrors a cautious stance against the backdrop of inflation reluctant to retreat, suggesting rates will remain elevated for the foreseeable future.

While markets hoped for signals of upcoming rate cuts, Chair Powell poured cold water on those expectations. In his recent remarks, he highlighted that inflation data "have come in above expectations," underscoring the need for a patient approach towards any potential easing of policy.

The central bank's latest comments also point to a slightly more optimistic view on economic risks, noting a shift towards a better balance between employment and inflation goals. Yet, Powell made it clear that the Fed is in no rush to declare victory over inflation or to hint at an end to rate hikes. Instead, the focus remains squarely on achieving the elusive 2% inflation target with minimal disruption.

Markets responded with cautious optimism: stocks and Treasuries edged higher, signaling relief, while futures recalibrated, tempering expectations for aggressive rate cuts. Additionally, the Fed's strategy to slow down the reduction of its hefty balance sheet aims to keep market jitters in check without stripping itself of the liquidity needed to tackle upcoming economic fluctuations.

As the economic landscape continues to evolve, the Fed’s latest policy maneuvers provide a telling glimpse into the challenges of steering the economy towards stable growth without igniting further inflationary spikes or stifling economic vitality.

History shows that the SPX has historically seen returns skewed to the upside on 1-month horizon, when rates have been held between 5.25% - 5.50% while 10Y yields have been above 4.6%

On a 1 month horizon, when rates are between 5.25 - 5.50% while 10Y yields are above 4.6%:

Top 3 Performing S&P Sectors:

Bottom 3 Performing S&P Sectors:

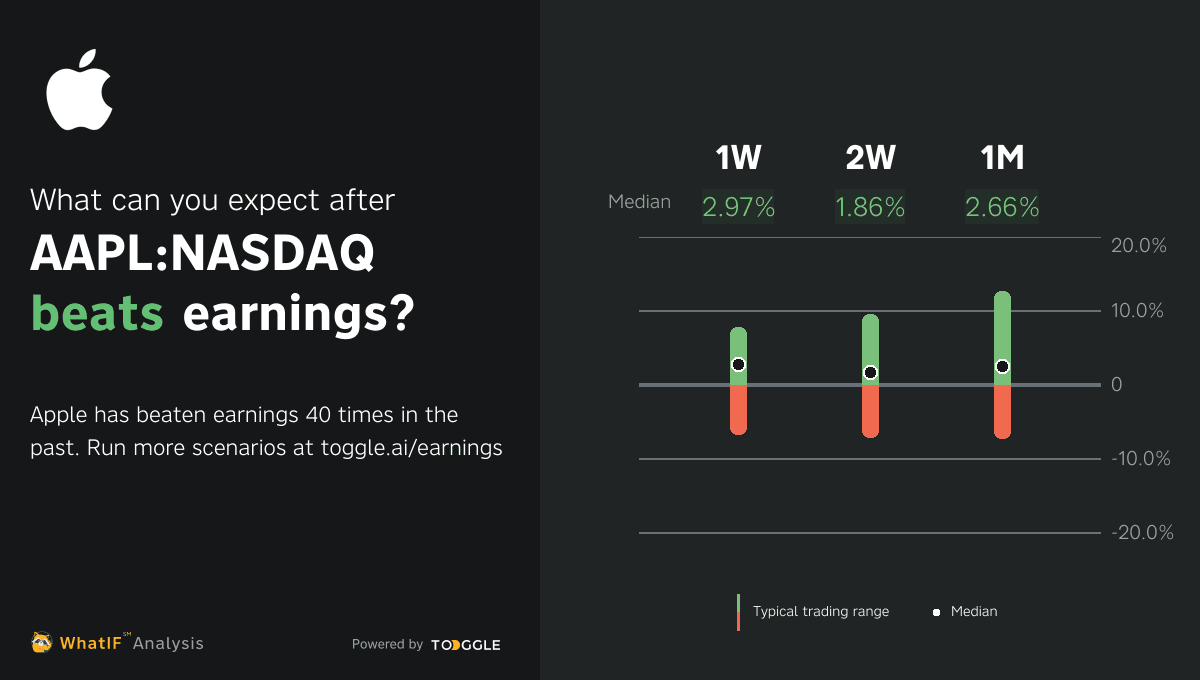

Apple is set to release its fiscal second-quarter earnings, with expected declines in both revenue and net income to $90.36 billion and $23.26 billion, respectively, compared to the same period last year. This anticipated drop follows the seasonal trend post-holiday quarter. Attention is on iPhone sales, especially in China where competition has intensified, with projections showing a decrease to 51.6 million units from 58 million.

Additionally, investors are looking for updates on Apple's AI strategy and potential financial maneuvers, including a proposed $90 billion buyback and a 3% dividend hike. Amid these developments, Apple's stock has fallen nearly 12% since the start of 2024.

Daily Brief - Fed Stands Firm

Up next

Dec 12

preview