Dec 12

preview

Toggle AI is now Reflexivity! Click here to go to our new website

TLDR: The Fed raised rates at the fastest clip in 40 years in 2022 and 2023 to fight inflation reaching a four-decade high. They finally stopped when the benchmark rate reached a range between 5.25% and 5.5% last July. But they have been veeeery slow in bringing the rates back down.

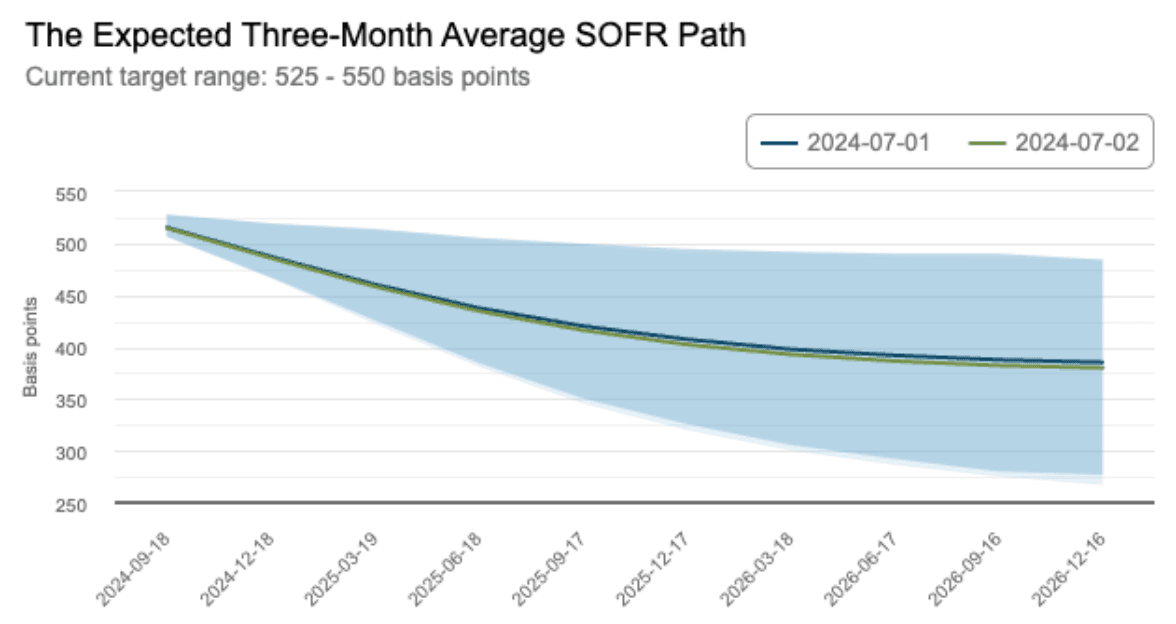

It’s not as if markets are banking on an aggressive cutting cycle: the current implied path of interest rate cuts is extremely … extremely … benign. 4% by the end of 2026? Wow. This is nothing like the aggressive pace we saw on the way up.

Why are they so reluctant to bring relief to the economy?

One - and possibly biggest - reason is the labor market. The Fed feels like it has time to cut interest rates so long as the labor market stays healthy. While payroll growth has been solid this year - as apparent in today’s slightly higher than expected payroll number - there are signs that consumer spending is finally slowing in line with what officials have long anticipated.

“You can see the labor market is cooling off, appropriately so, and we’re watching it very carefully,” Powell said. He repeated his view that a sudden deterioration in employment growth could spur a faster turn to rate cuts.

For a while, it was shelter inflation. And then energy. But right now, the Fed’s focus is squarely on the labor market: jobless claims, payroll prints, wage inflation … that’s where you need to look if you are keen to understand when (and how much) the Fed will cut rates. The number today isn’t going to change their view. Yes, the unemployment rate is a tad higher but not nearly enough to move away from the central case of “maybe one little cut by year end” espoused in Fed communications in recent months.

Markets have come to terms with the fact that cuts may have to wait until next year. Besides, soon we will have an election to try and price.

The chart above shows the historical 6-month response from the S&P 500 post previous US Elections - look out for potential downside risk in the near term!

Here is the historical response from S&P sectors on a 6-month horizon, following a US election:

Daily Brief - A rate cut in 2024, or 2025?

Up next

Dec 12

preview