Dec 12

preview

Toggle AI is now Reflexivity! Click here to go to our new website

TLDR: Stock markets in the East have shown a promising start to the week, as global investors turn their focus towards a critical corporate earnings and economic data.

As of Monday, benchmarks across Japan, Australia, and South Korea have each risen by atleast 1%. This rise marks a partial recovery from the declines experienced last week, spurred by a mixture of Middle Eastern geopolitical tensions and policy comments from the U.S. Federal Reserve.

The slight weakening of the U.S. dollar has also contributed to the positive mood, as fears of escalation in Middle Eastern conflicts have not materialized further.

Investors globally are gearing up for a week heavy with implications for monetary policy direction. Notable releases include U.S. economic growth figures and the Fed’s preferred inflation measure.

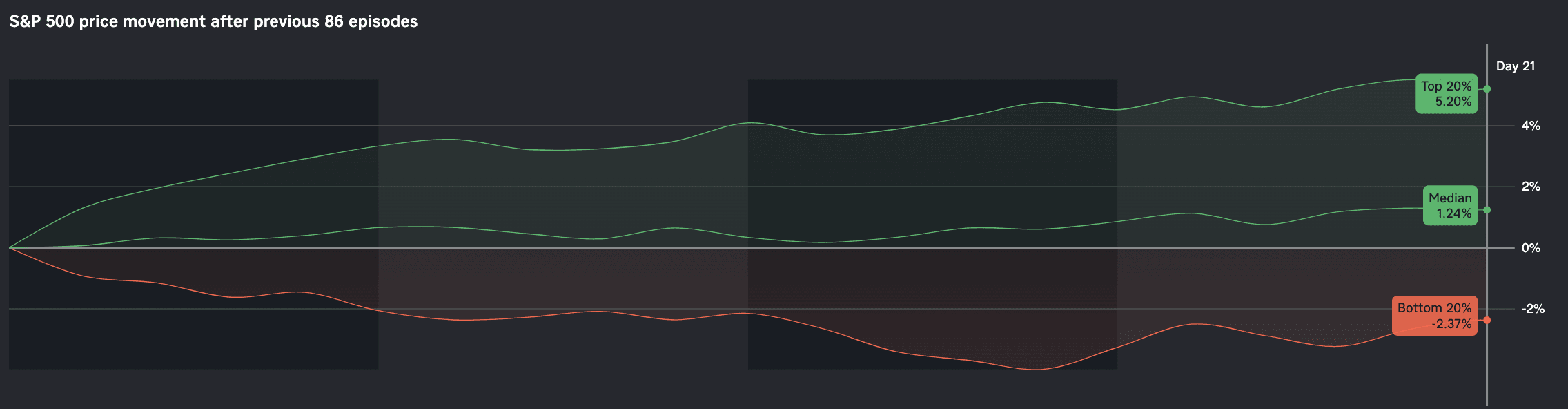

The S&P 500 has faced challenges, recording its worst performance since March 2023 last week - dropping more than 5% from its all-time peak.

This week, over half of the "Magnificent Seven” are set to release their earnings reports, raising investor curiosity about whether these firms will meet the lofty expectations surrounding artificial intelligence.

As American markets prepare to open, the performance of Asian stocks offers a tentative but hopeful sign.

The chart above show the S&P's median 1 month performance following the past 86 instances when the index experienced a significant decline similar to last week.

Here are the historically best and worst performing US sectors on a 1-month horizon:

Top 3 Performing Assets:

Bottom 3 Performing Assets:

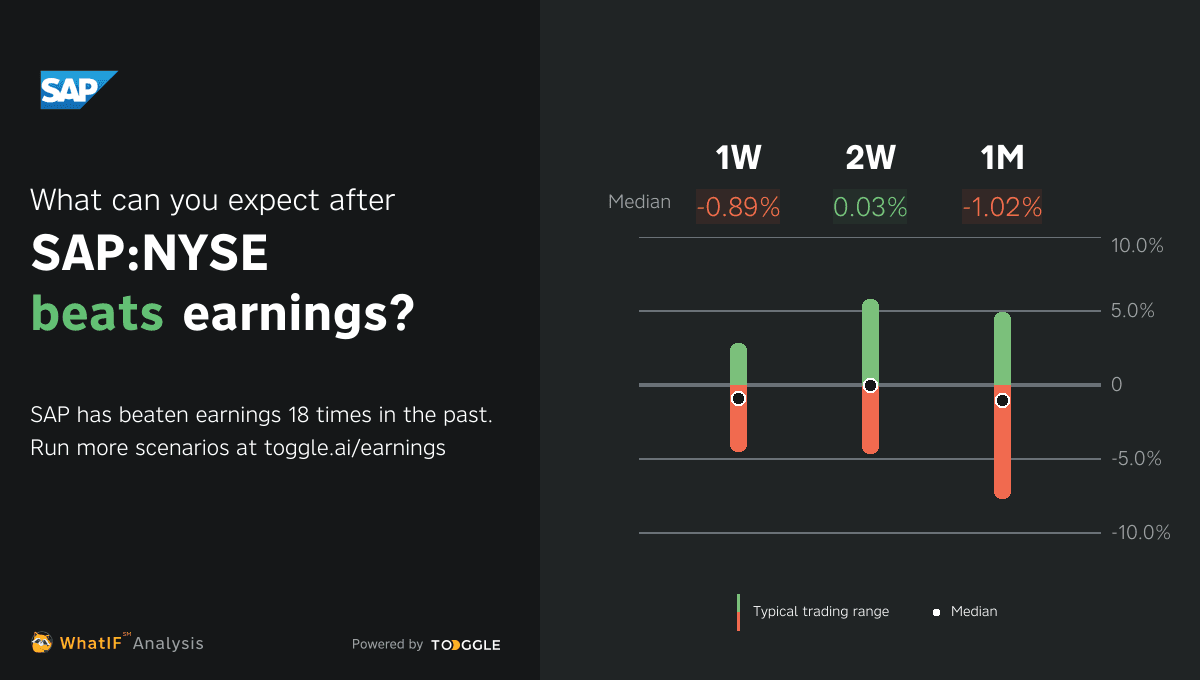

SAP SE is set to report its earnings for the most recent quarter, with analysts anticipating earnings per share of €0.985, a decline from last year's same-quarter earnings of €1.27 per share. Additionally, Wall Street forecasts the company's revenue to reach €8.02 billion, marking a 7.74% increase from the previous year.

Looking ahead to the full fiscal year, earnings per share are expected to rise significantly to €4.92 from €2.21, with overall revenue projected to increase to €33.85 billion from €31.21 billion last year.

Daily Brief - Rising in the East

Up next

Dec 12

preview