Dec 12

preview

Toggle AI is now Reflexivity! Click here to go to our new website

TLDR: Netflix (NFLX) delivered a striking first-quarter performance, significantly surpassing Wall Street expectations with a robust increase in both revenue and subscriber count.

The streaming giant added an impressive 9.3 million subscribers in the first quarter, dwarfing analyst predictions of 4.8 million and building on the 13 million net additions in the previous quarter.

This growth in subscribers reflects a continued demand for the service despite increasing competition in the streaming sector.

Financially, Netflix reported revenues of $9.37 billion, a 14.8% rise from the previous year. This revenue bump was supported by several strategic moves by Netflix, including a crackdown on password sharing, introduction of an ad-supported subscription tier, and recent hikes in subscription prices in certain markets.

Earnings per share (EPS) for the quarter were particularly strong at $5.28, well above the consensus estimates of $4.52 and nearly double the EPS of $2.88 from the same quarter last year.

However, not everything in the report spelled smooth sailing for Netflix. The company's guidance for second-quarter revenue of $9.49 billion was slightly below the expected $9.51 billion, leading to a more than 3% drop in the stock price in after-hours trading.

Additionally, Netflix announced a significant change in its reporting strategy. Starting next year, the company will no longer report quarterly membership numbers or average revenue per member.

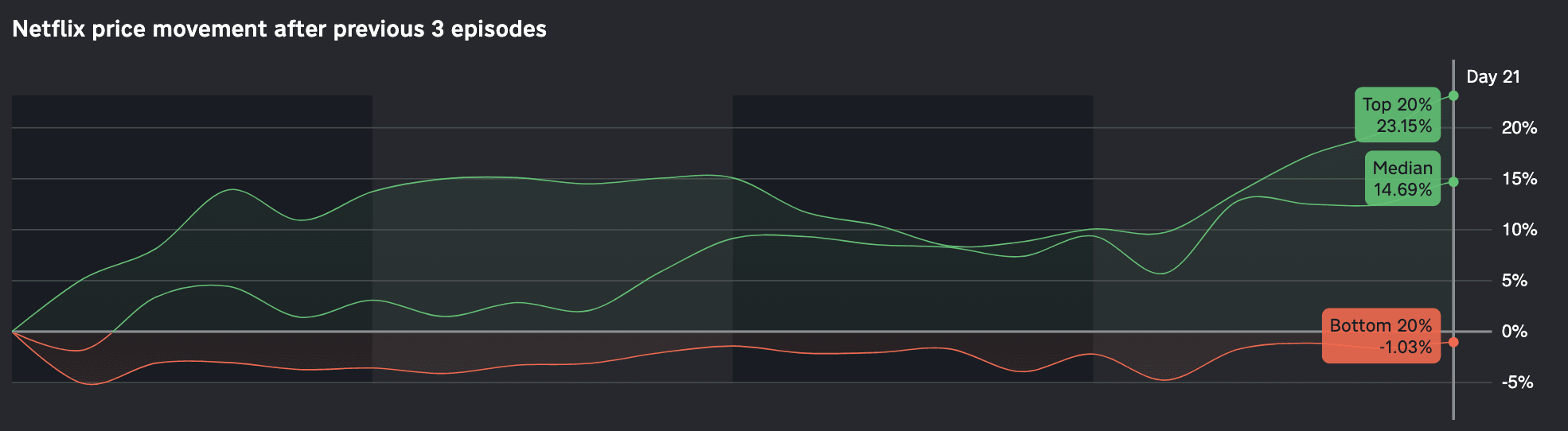

The chart above shows the historical 1 month response from Netflix stock post the past 3 instances when Netflix has beaten earnings expectations by $0.76 or more.

Here is the historical 1-month response from Netflix peers when the company has previously beaten earnings by $0.76 or more.

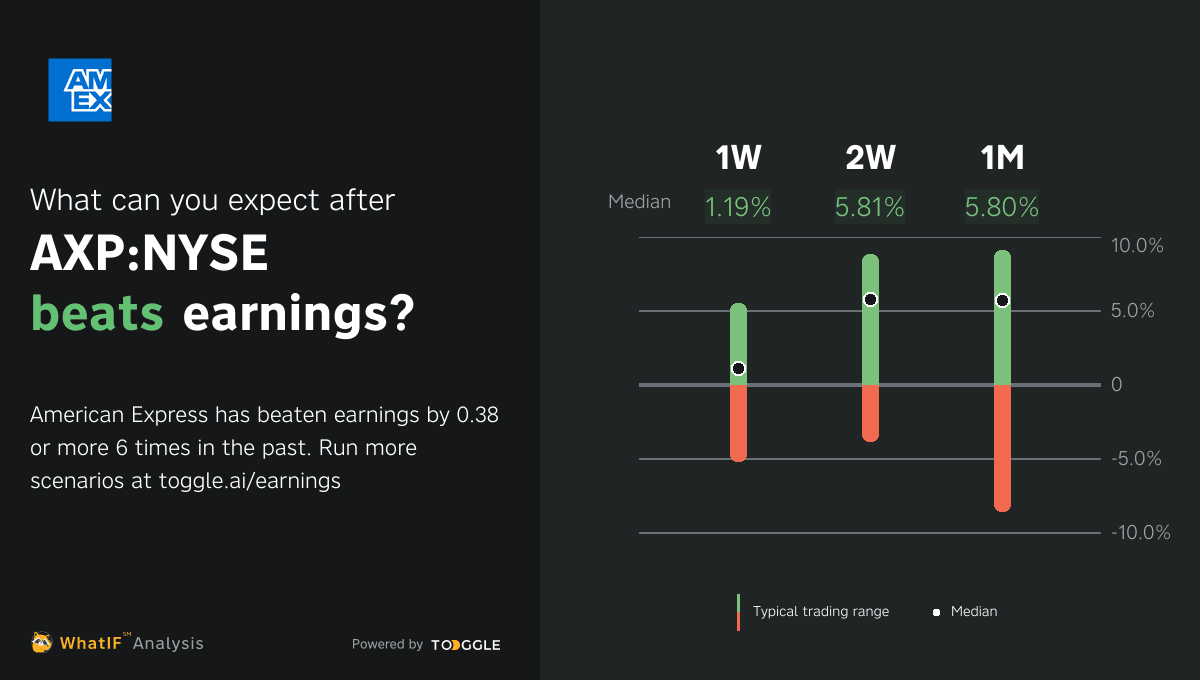

American Express reported increased first-quarter earnings, with net income rising to $2.4 billion, or $3.33 per share, up from $1.8 billion a year earlier. Revenue grew to $15.8 billion from $14.3 billion.

This growth was driven by a 7% rise in cardmember spending, adjusted for foreign exchange. The company's results exceeded analyst expectations, which had forecasted earnings of $2.95 per share on $15.8 billion in revenue.

Daily Brief - Streaming Success

Up next

Dec 12

preview